What Is The Minimum Payment On A Balance Transfer Credit Card

adminse

Mar 31, 2025 · 9 min read

Table of Contents

Decoding the Minimum Payment on a Balance Transfer Credit Card: Discoveries and Insights

What are the hidden costs and implications of only paying the minimum on a balance transfer credit card?

Understanding minimum payments is crucial for successfully managing debt and avoiding the pitfalls of high interest charges.

Editor’s Note: This article on minimum payments for balance transfer credit cards was published today.

Why Understanding Minimum Payments Matters

Balance transfer credit cards offer a potentially powerful tool for managing debt. By transferring high-interest debt to a card with a 0% introductory APR period, consumers can save significantly on interest charges. However, the effectiveness of this strategy hinges heavily on understanding and managing the minimum payment requirement. Failure to do so can quickly negate the benefits and even lead to a worse financial situation than before the transfer. Understanding minimum payment calculations, implications of only paying the minimum, and strategies for responsible repayment are crucial for successful debt management. This knowledge directly impacts personal finances, credit scores, and overall financial well-being.

Overview of the Article

This article delves into the complexities of minimum payments on balance transfer credit cards. We will explore how minimum payments are calculated, the significant impact of paying only the minimum, strategies for accelerated repayment, the potential risks associated with minimum payments, and frequently asked questions to clarify any uncertainties. Readers will gain a comprehensive understanding of this crucial aspect of balance transfer cards and acquire actionable insights to manage their debt effectively.

Research and Effort Behind the Insights

The insights presented in this article are based on extensive research, encompassing analysis of credit card agreements from major issuers, examination of industry reports on consumer debt, and consultation of financial literacy resources. The information is presented in a clear and concise manner, focusing on practical applications and avoiding overly technical jargon.

Key Takeaways

| Key Point | Description |

|---|---|

| Minimum Payment Calculation | Varies by issuer; typically a percentage of the balance (e.g., 1-3%), or a fixed minimum (e.g., $25). |

| Impact of Only Paying the Minimum | Prolongs repayment period, significantly increases total interest paid over time, and can negatively impact credit scores. |

| Strategies for Accelerated Repayment | Paying more than the minimum, budgeting effectively, exploring debt consolidation options, and seeking professional financial advice. |

| Risks Associated with Minimum Payments | High interest accumulation, potential for exceeding credit limits, negative impact on credit utilization ratio, and potential for default. |

| Importance of Understanding Agreements | Carefully review the credit card agreement to understand the specific terms and conditions regarding minimum payments and interest rates. |

Let’s dive deeper into the key aspects of minimum payments on balance transfer cards, starting with how these minimums are calculated.

Exploring the Key Aspects of Minimum Payments

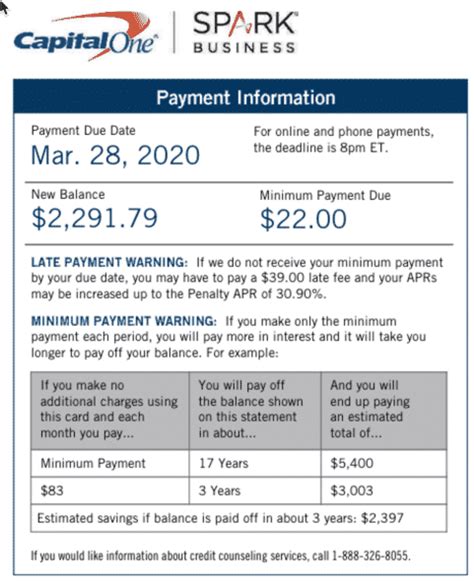

1. Calculating the Minimum Payment: The minimum payment on a balance transfer credit card isn't a standardized figure. It varies depending on the card issuer, the outstanding balance, and the terms outlined in the credit card agreement. Generally, the calculation involves either a percentage of the balance (typically between 1% and 3%) or a fixed minimum dollar amount (often around $25-$35). Some issuers might use a combination of both methods, ensuring a minimum payment of at least a certain percentage or dollar amount, whichever is greater. It's crucial to consult your card's agreement to understand the exact calculation method.

2. The High Cost of Minimum Payments: While paying only the minimum payment seems convenient, it's financially detrimental in the long run. The primary reason is that a significant portion of your monthly payment goes towards interest, leaving only a small fraction to reduce the principal balance. This extends the repayment period dramatically, resulting in considerably higher total interest charges. Consider this example: A $5,000 balance at 18% APR could take decades to repay with minimum payments alone, accumulating thousands of dollars in interest. In contrast, paying even a slightly higher amount each month accelerates the repayment and significantly reduces the overall interest paid.

3. Impact on Credit Scores: Paying only the minimum payment can negatively impact your credit score. Credit scoring models consider your credit utilization ratio, which is the percentage of available credit you're currently using. Consistently paying only the minimum keeps your credit utilization high, signaling to lenders that you might be struggling to manage your debt. A lower credit score can make it harder to obtain future loans, secure favorable interest rates, and even qualify for certain services.

4. Strategies for Accelerated Repayment: To avoid the pitfalls of minimum payments, proactive strategies are essential. These include: budgeting meticulously to allocate extra funds toward debt repayment; making payments more frequently (e.g., twice a month); exploring debt consolidation options to combine multiple debts into one with a lower interest rate; and seeking guidance from a financial advisor for personalized strategies.

5. Avoiding Common Pitfalls: Many individuals fall into the trap of believing that as long as they make the minimum payment, they are financially responsible. However, this couldn't be further from the truth. Ignoring the implications of minimum payments often leads to debt snowballing, impacting financial stability. Always carefully review your credit card agreement, understand the calculation of your minimum payment, and develop a responsible repayment plan.

Closing Insights

The minimum payment on a balance transfer credit card, while seemingly innocuous, is a crucial factor that profoundly impacts the overall debt repayment process. Understanding how it’s calculated, the significant cost of only meeting this minimum, and the available strategies for accelerated repayment is fundamental to successful debt management. Failing to address these aspects can lead to prolonged debt, substantially higher interest payments, and a negative effect on credit scores. By adopting a proactive approach and understanding the implications, individuals can effectively leverage balance transfer cards to manage debt and achieve financial stability.

Exploring the Connection Between Credit Utilization and Minimum Payments

Credit utilization is the percentage of your available credit you are using. A high credit utilization ratio negatively impacts your credit score. Paying only the minimum payment on a balance transfer card directly contributes to a higher credit utilization ratio because the balance remains elevated for a longer period. Lenders view high credit utilization as a sign of potential financial instability. The minimum payment calculation itself doesn’t directly determine credit utilization, but the consistent reliance on minimum payments results in a higher utilization rate, impacting credit scores negatively. For example, if a card has a $10,000 limit and the balance consistently remains around $8,000 due to minimum payments, the credit utilization would be 80%, a very high percentage. This can significantly lower your credit score.

Further Analysis of Interest Accrual

Interest accrual is the accumulation of interest charges on your outstanding balance. When only making the minimum payment, a much larger portion of the monthly payment goes toward interest rather than the principal balance. This causes interest to continue accumulating on the remaining principal, creating a cycle where debt takes significantly longer to repay. Let's illustrate this with a simple example: Imagine a $10,000 balance with a 15% APR. The minimum payment might only cover the accruing interest, leaving the principal untouched. This means you're paying interest on the initial $10,000 for an extended period, incurring substantially higher overall costs. Conversely, paying more than the minimum significantly reduces the principal, thereby lowering the amount of interest charged in subsequent months.

FAQ Section

1. Q: What happens if I miss a minimum payment on my balance transfer card?

A: Missing a minimum payment can result in late fees, increased interest rates, a negative impact on your credit score, and potential damage to your credit rating.

2. Q: Can I negotiate a lower minimum payment with my credit card company?

A: It's unlikely, but you can attempt to contact your credit card issuer and explain your financial situation. They may offer options, such as a hardship program, but there's no guarantee.

3. Q: How does the minimum payment calculation differ between balance transfer cards and regular credit cards?

A: The calculation method is generally similar; however, specific percentages or fixed minimums can vary between issuers and card types. Always refer to your specific card agreement.

4. Q: Does paying more than the minimum payment improve my credit score?

A: Yes, consistently paying more than the minimum reduces your credit utilization, which positively affects your credit score.

5. Q: What is the best way to manage my balance transfer card to avoid high interest charges?

A: The best approach is to pay as much as possible, ideally more than the minimum payment, to pay down the principal balance as quickly as possible.

6. Q: Should I always choose the balance transfer card with the lowest minimum payment?

A: No. Focus on the overall APR and repayment terms rather than solely on the minimum payment. A lower minimum payment might seem appealing but can lead to prolonged debt and higher interest charges in the long run.

Practical Tips

-

Understand your credit card agreement: Thoroughly read the terms and conditions to understand the minimum payment calculation and other key details.

-

Create a budget: Allocate a specific amount each month towards your balance transfer card repayment.

-

Pay more than the minimum: Make extra payments whenever possible to accelerate your debt repayment.

-

Set up automatic payments: Automate payments to ensure you consistently meet the minimum payment and avoid late fees.

-

Monitor your credit utilization: Track your credit utilization ratio to ensure it remains low.

-

Explore debt consolidation options: Consider consolidating your debts into a single loan with a lower interest rate.

-

Seek professional financial advice: Consult a financial advisor for personalized debt management strategies.

-

Avoid additional charges: Refrain from making new purchases on the card while carrying a balance.

Final Conclusion

The minimum payment on a balance transfer credit card is not merely a suggested payment; it's a critical component influencing your financial health. Understanding its intricacies, potential pitfalls, and strategic approaches to repayment is essential for successfully managing debt and achieving financial well-being. While balance transfer cards offer attractive opportunities for debt management, neglecting the importance of understanding minimum payments can negate the benefits and even exacerbate the debt problem. By adopting the strategies outlined in this article, individuals can take control of their finances and navigate the complexities of balance transfer cards effectively. Remember, proactive planning and a commitment to responsible repayment are key to achieving long-term financial success.

Latest Posts

Latest Posts

-

Payment For Target

Apr 02, 2025

-

Target Method Of Payment

Apr 02, 2025

-

Perkins Loans

Apr 02, 2025

-

Perkins Loan Definition

Apr 02, 2025

-

What Is The Minimum To Pay On A Credit Card

Apr 02, 2025

Related Post

Thank you for visiting our website which covers about What Is The Minimum Payment On A Balance Transfer Credit Card . We hope the information provided has been useful to you. Feel free to contact us if you have any questions or need further assistance. See you next time and don't miss to bookmark.